Dubai Bank Account Rejected? Shocking Reasons & Fixes (2026)

Dubai is one of the world’s easiest places to set up a company—fast licensing, modern free zones, and an investor-friendly ecosystem. Yet in 2026, there’s one problem that keeps ruining launch plans for entrepreneurs, NRIs, founders, and even established foreign companies:

Dubai bank account rejected.

And here’s the painful part: most applicants only find out after spending money on company formation, visas, office rent, and legal documentation. At Wings9, we’ve seen companies fully licensed—but unable to trade for weeks because banking didn’t go through.

So let’s expose the real reasons UAE banks reject applications in 2026—and how to avoid them like a pro.

Quick Answer

If your Dubai bank account rejected application happens, it’s usually due to incomplete KYC documents, unclear business activity, weak source-of-funds proof, high-risk nationality/activity flags, mismatch between license and operations, or no UAE business substance. The solution is preparing a bank-ready file with strong compliance documentation and a clear transaction story.

Why Bank Rejections Are Increasing in Dubai (2026 Reality)

Banking in Dubai is not “difficult”—it’s compliance-driven.

UAE banks are under strong pressure to follow:

AML (Anti-Money Laundering) controls

KYC (Know Your Customer) checks

UBO (Ultimate Beneficial Owner) disclosures

FATF-aligned governance expectations

This is why UAE bank account opening problems have increased—especially for first-time residents, Free Zone companies, and foreign-owned businesses.

Wings9 reality check: In 2026, your company’s compliance profile matters as much as your business idea.

The #1 Mistake: Treating Banking as the Last Step

Many founders do this:

Setup company

Apply visa

Rent office

“Now we’ll open a bank account.”

But banks evaluate:

business model credibility

operational substance

ownership transparency

expected transaction behaviour

If the bank doesn’t “understand” your business on paper, the outcome is predictable: a Dubai bank account rejected.

Shocking Reasons Dubai Bank Accounts Get Rejected (2026 List)

Below are the most common reasons we see in real Wings9 cases.

1) Your Business Activity Looks High-Risk to the Bank

Banks classify certain activities as higher AML risk, including:

crypto-related services

money services

general trading without clarity

import/export with unclear suppliers

marketing services linked to foreign payments

Even legitimate businesses can trigger screening if the wording is vague.

Fix: Choose licensing activities strategically and prepare invoices/contracts early.

2) Mismatch Between Trade License and Actual Business

This is one of the biggest KYC issues that UAE banks highlight.

Example:

License says “computer systems consultancy.”

Applicant describes business as “online trading.”

Website shows “crypto education.”

This mismatch makes banks think:

“What are you really doing?”

Result: Dubai corporate bank account rejection.

Fix: Align license activity + website + pitch + contract proofs.

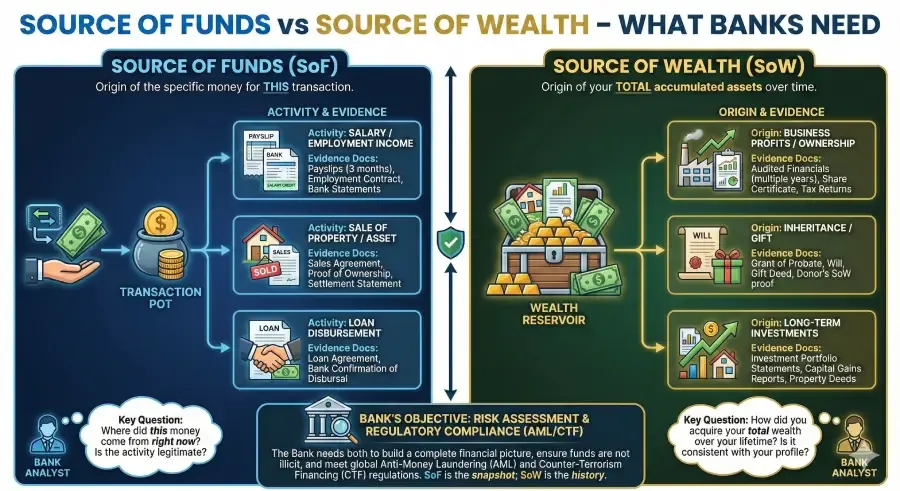

3) Weak Source of Funds / Source of Wealth Proof

Banks must know where your money comes from.

If your profile says:

investor

freelancer

entrepreneur

But you can’t show:

income statements

tax returns

dividends proof

business sale documents

Then it’s high-risk for them.

Fix: Provide a clear source-of-funds pack (more below).

4) Your UBO / Ownership Structure Is Unclear

If your structure includes:

multiple shareholders

overseas holding companies

nominee arrangements

unclear UBO documentation

Banks will delay or reject.

Under UAE rules, UBO transparency is mandatory, and banks cross-check this heavily.

Fix: Make UBO documentation clean and consistent across all filings.

5) No Proof of UAE Business Substance

In 2026, “paper companies” struggle.

Banks look for:

UAE office lease (Ejari or Free Zone facility contract)

active visa(s)

local phone number

business presence evidence

If your company has no physical footprint, the bank assumes it may be set up just for account access.

Fix: Build substance before applying (Wings9 guide below).

6) Poor Website / No Digital Footprint (Yes, This Matters)

This shocks people.

If the bank searches your company and finds:

no website

website under construction

gmail-only email

no service description

unclear contact details

They will consider it non-credible.

Fix: Build a clean professional site + branded email.

7) Nationality or Country-of-Operation Risk Flags

Some applicants face enhanced screening due to:

nationality

Business links to sanctioned jurisdictions

frequent high-value international transfers

Banks may not openly say it, but it impacts decisions.

Fix: Work with the right bank and prepare a stronger compliance file.

8) You Applied Too Early (Before Visa / Emirates ID)

For many banks, the order matters.

If you apply without:

Emirates ID

visa stamping

tenancy contract

Approval becomes harder.

Fix: We follow the correct timeline to reduce rejection risk.

9) You Don’t Have Contracts or Invoices Ready

Banks want proof of actual business activity.

Examples of accepted evidence:

signed client agreements

supplier contracts

purchase orders

expected monthly invoice estimates

Without this, your application looks theoretical.

Fix: Prepare a transaction profile document (Wings9 template).

10) Badly Prepared Bank Application Form

This sounds minor—until you see how banks interpret it.

Common mistakes:

Incorrect expected revenue

Wrong transaction countries

unclear purpose of the account

inconsistent shareholder info

Result: reasons for Dubai bank account rejection become self-created.

Fix: Apply with a complete bank-ready file.

Checklist: Bank-Ready Documentation (2026)

If you want approval, your file must be “compliance-ready”.

For Company Accounts (Corporate)

Trade license + MOA

Shareholder passport copies

Visa + Emirates ID

Office lease/facility agreement

UBO declaration

Company profile + business plan

Client/supplier contracts

Invoices (if available)

Source of funds + source of wealth proofs

For Personal Accounts

UAE residence visa + Emirates ID

Salary certificate/employment letter (if applicable)

Bank statements (last 6 months)

Tax returns or income proof

Address proof

This is how you avoid the common cycle: Dubai bank account rejected → reapply → rejected again.

Mainland vs Free Zone: Does It Affect Bank Approval?

Yes—slightly.

Mainland Companies

tend to have stronger “local market” logic

Office/Ejari helps substance

often easier for service and retail businesses

Free Zone Companies

totally bankable in 2026

but need stronger documentation

must show substance and real trade logic

This ties directly into our main pillar guide:

👉 https://wings9.ae/company-formation-in-dubai-2026-mainland-vs-free-zone/

Wings9 Pro Tip:

If your core market is the UAE, mainland reduces friction. If global, Free Zone works—just build a stronger compliance file.

Featured Snippet Table: Why UAE Banks Reject Accounts

Reason | What Bank Thinks | Wings9 Fix |

|---|---|---|

Weak KYC documents | “Risk: unknown profile.” | Complete compliance pack |

No substance | “Paper company” | Office + visa alignment |

Activity mismatch | “Not credible/unclear.” | Align licence + business |

No source of funds | “Suspicious income” | SOP/SOW documentation |

No contracts | “No real business” | Prepare transaction evidence |

Poor website | “Not legitimate” | Professional digital footprint |

Wrong bank selection | “High-risk segment” | Match profile to bank |

How to Avoid Bank Account Rejection in the UAE (Wings9 System)

Here’s the exact approach we follow for higher approval probability:

Step 1: Create a “Transaction Story”

Banks want clarity:

What you sell

Who pays you

from which countries

expected ticket size

number of transfers per month

Step 2: Align Legal Documents

Ensure:

activity matches operations

MOA matches reality

UBO details match across authorities

Step 3: Build Substance Signals

office lease / flexi-desk agreement

active visa

UAE contact details

working website

Step 4: Apply to the Right Bank

Not every bank is right for every business.

Wings9 Insight:

Many rejections aren’t because the applicant is “bad”. They’re because the bank is the wrong match for the profile.

What to Do If Your Dubai Bank Account Is Rejected

Don’t panic. Don’t spam applications. That makes it worse.

Do this instead:

ask for rejection reason (if possible)

fix the compliance gap

Rebuild the file

switch bank strategy if needed

At Wings9, we treat rejection as:

a compliance signal, not a dead-end.

FAQ

1) Why is my Dubai bank account rejected?

Most rejections happen due to incomplete KYC, unclear business model, lack of source-of-funds proof, or no UAE business substance.

2) Can Free Zone companies open corporate bank accounts in Dubai?

Yes. Free Zone companies can open accounts, but banks require stronger compliance documentation and clear operational proof.

3) How long does it take to open a corporate bank account in Dubai?

It typically takes 2–6 weeks, depending on the bank, shareholder nationality, compliance profile, and document readiness.

4) Does a UAE residence visa help with bank approval?

Yes. Having a visa and an Emirates ID significantly improves bank approval probability.

5) What documents do UAE banks require for business accounts?

Trade licence, MOA, passports, UBO details, proof of address, office lease/facility contract, contracts/invoices, and source-of-funds proof.

6) What is the best way to avoid UAE bank account rejection?

Prepare a bank-ready file with complete KYC, UBO clarity, source-of-funds evidence, and a clear transaction profile before applying.

7) Can Wings9 help after rejection?

Yes. Wings9 reviews the rejection, identifies compliance gaps, rebuilds documentation, and re-applies strategically with the right bank.

Pillar Page Integration

Bank approval success starts with choosing the correct structure. If you’re still deciding Free Zone vs mainland, start here:

👉 https://wings9.ae/company-formation-in-dubai-2026-mainland-vs-free-zone/

This article is a high-intent sub-topic under that pillar because banking is the #1 operational bottleneck after setup.

Wings9 2026 Outlook (Unique Takeaway)

Here’s what we predict for 2026 (and most agencies won’t tell you):

UAE banks will increasingly approve businesses that look compliance-ready, not just “licensed.”

Meaning:

Strong documentation wins

structured transaction logic wins

substance wins

transparency wins

So the future isn’t about finding the “easiest bank.”

It’s about becoming the cleanest file.

That’s how you ensure your Dubai dream doesn’t get stuck at:

Dubai bank account rejected.

Want approval without delays?

We at Wings9 Management Consultants help entrepreneurs and foreign investors build a complete bank-ready profile—before the application goes in.

Start your Dubai journey with Wings9.